You've probably heard about the recent tax bill the "One Big Beautiful Bill Act", also known as OBBBA.

It's arguably one of the biggest, and most anticipated, tax bills since the Tax Cuts and Jobs Act (TCJA) in 2017. OBBBA was highly anticipated because a lot of the favorable tax provisions (increased standard deductions, lower tax rates, QBI deduction, etc.) in TCJA were set to expire at the end of this year, 2025. So many people were expecting some sort of legislation prior to the end of the year to address the expiration of these provisions and were very curious as to what any potential new legislation would look like.

Well the wait is over.

OBBBA was introduced on July 4th of this year, which was actually very convenient that the bill was introduced in the middle of the year giving tax payers and planners plenty of time to understand the details of the bill and do any necessary tax planning before year end. While the bill is very long and we won't cover everything in the bill here, we will discuss some of the most important aspects of the bill for individuals and families as they save, invest, build for the future and prepare for retirement. But, before we dive in, it's important to note that a lot of the bill is keeping things the same, with some new things, that will likely end up not changing what you owe in taxes that much in 2025 compared to 2024 and earlier tax years.

Let's dive in. So what's in OBBBA?

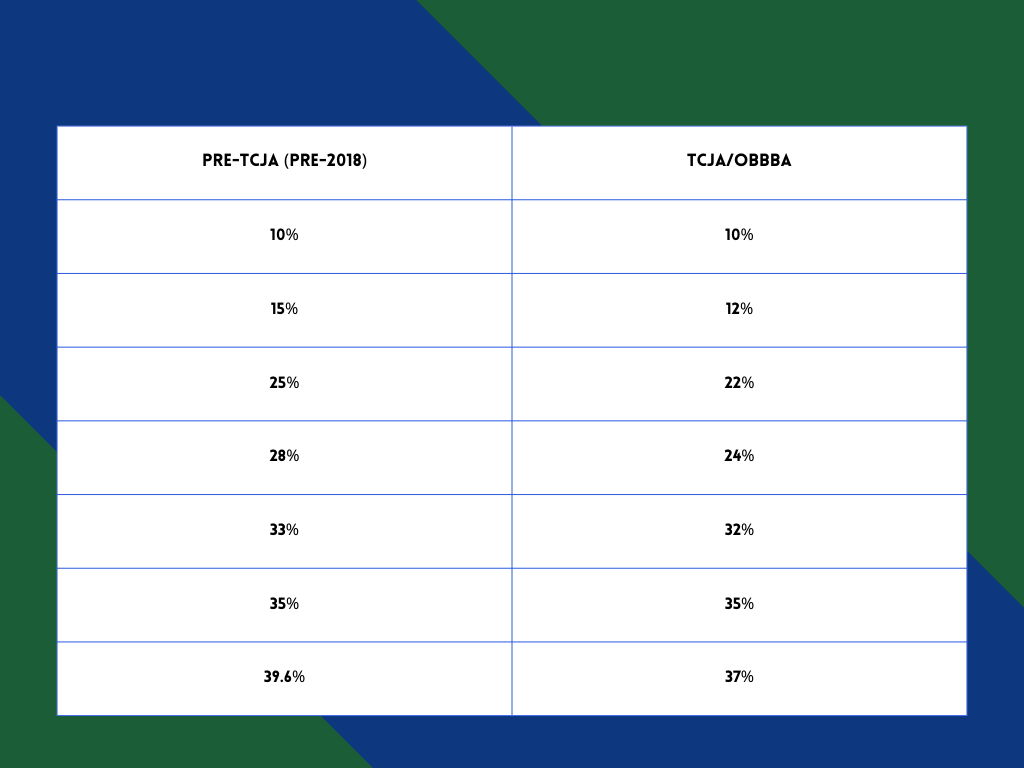

First and foremost, the new OBBBA tax bill makes permanent the reduced income tax brackets that TCJA introduced back in 2018. The now permanent (unless there's additional legislation that changes these tax brackets again) income tax brackets are below along with the higher pre-TCJA tax rates.

TCJA reduced nearly all income tax brackets, with the exception of the 10% and 35% brackets, and had OBBBA not been passed in July then tax rates were set to revert back to the old Pre-TCJA higher tax brackets. OBBBA will keep tax rates lower for the foreseeable future.

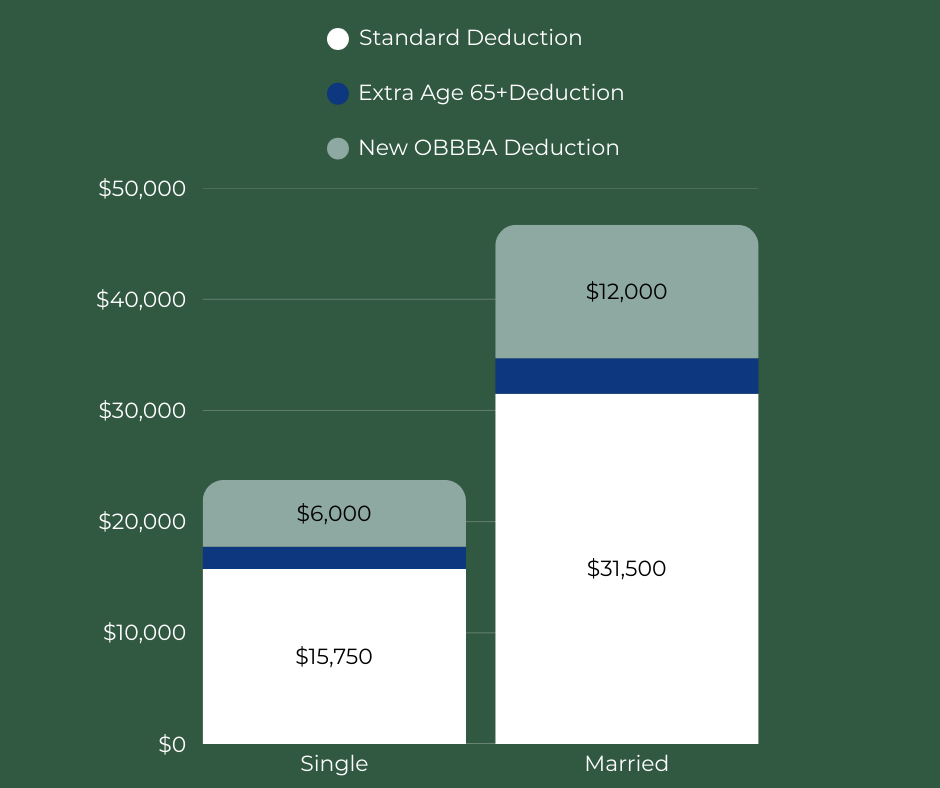

OBBBA makes permanent the increased standard deduction introduced in 2018 by TCJA. Had OBBBA not been passed the standard deductions were set to revert back to their higher, pre-TCJA levels. But the new tax bill has made those standard deduction increases permanent and adjusted each year for inflation.

The now standard deductions for 2025 under OBBBA are:

Single - $15,750

Head of Household - $22,500

Married Filing Jointly - $31,500

There was a lot of talk leading up to the bill's release about not taxing social security benefits (currently up to 85% of your social security benefit can be taxable). And while OBBBA didn't directly get rid of the tax on social security it did create an additional personal deduction for seniors age 65 + that they can use to offset up to $6,000 of their income. This will help limit the overall impact of your social security benefit on your overall tax liability.

However, this deduction is, right now, only temporary with it set to expire after 2028.

This deduction has income phaseouts at $175,000 for single filers ($250,000 for married filing joint) so once you exceed the income threshold you won't be able to claim the deduction.

Something nice about this provision is that for married couples filing jointly, both spouses can each take the $6,000 deduction.

Moreover, this deduction is on top of the standard deduction and the extra age 65+ deduction ($2,000 for single and $3,200 for married filing joint) resulting in an additional $6,000 deduction for single filers and $12,000 deduction for married taxpayers.

You can either take the higher of the standard deduction or itemized deduction and if you itemize there are some changes with OBBBA.

State and Local Tax (SALT) Deduction

One of the biggest complaints with the TCJA was that it limited the amount of SALT you can deduct. Currently there's a $10,000 cap on the SALT deduction; however, OBBBA temporarily increased the $10,000 cap to $40,000 for 2025. For years 2026-2029 the $40,000 limit is set to increase 1% each year with the limit reverting back to the $10,000 cap in 2030. The new limit is also the same for single and married filing jointly tax payers.

But there are some income limits to be able to take advantage of the increased $40,000 cap.

Once your modified adjusted gross income (MAGI) reaches $500,000 then the deduction begins to phaseout and then completely phases out once your MAGI reaches $600,000. The $500,000 MAGI threshold also increases each year from 2026-2029.

Even with the MAGI restrictions there should still be more taxpayers itemizing and taking advantage of the SALT deduction with the cap increase.

Mortgage Insurance Premiums

Mortgage insurance premiums are now deductible beginning in 2026 as part of the mortgage interest itemized deduction. Mortgage insurance is typically paid by the borrower when they owe more than 80% of their loan-to-value (LTV) and can easily be a couple hundred bucks a month as part of their mortgage payment.

The deductibility of mortgage interest is still limited to $750,000 in mortgages on your primary residence.

Charitable Contributions Deduction

Making donations to qualified charities has long been an itemized deduction, subject to Adjusted Gross Income (AGI) limitations as well as being dependent on what is being donated (cash, property, etc.) and to what kind of charity it's being donated to (public vs. non-public).

Cash donations made to public charities are deductible up to 60% of AGI, and non-cash contributions are deductible up to 50% (when using the cost basis for deduction) and up to 30% (when using the fair market value [FMV] for the deduction).

For other charities and organizations cash donations are deductible up to 30% of AGI and non-cash donations up to 20% of AGI (whether using cost basis or FMV for deduction).

*any donations above the AGI limitation can potentially be carried over to subsequent tax years.

What OBBBA changed with charitable contributions for itemized deductions is that there's now a floor of 0.5% of AGI to be able to take the deduction, starting in 2026. What this means is that deductions are only allowed if they exceed 0.5% of AGI (similar to the 7.5% AGI floor for itemized medical expenses).

For example, if your AGI is $300,000 then your charitable donations need to be above $1,500 ($300,000 x 0.5%) to be deductible. If you wanted to make a $30,000 cash donation then $28,500 is deductible. Also, if you contribute more than the upper AGI limit (30% of AGI for stock given to public charities for example), then the excess is carried forward to the following tax year as well as the amount of the donation reduced by the 0.5% AGI floor.

For example, if you had $300,000 of AGI and made a gift of stock worth $100,000 to your church, then $98,500 would be deductible due to the 0.5% AGI floor. However, only $90,000 ($300,000 x 30% = $90,000) would actually be allowable as a deduction in the current year because of the AGI limit of 30% for FMV property. The remaining $8,500 ($98,500-$90,000) plus $1,500 (amount of donation reduced by the 0.5% AGI floor) for a total of $10,000 would be carried forward to the next tax year for possible charitable donation deductions.

As you can see, this area gets very nuanced and detailed and thus it's important to work with a tax professional to help you plan around any charitable giving strategies.

Miscellaneous Itemized Deductions

TCJA eliminated these deductions temporarily and OBBBA eliminated them permanently.

These miscellaneous deductions included investment expenses (like advisory fees paid to investment advisors) and unreimbursed business expenses.

Limitations for High Earners in the 37% tax bracket

Before TCJA, high earners were subject to the "Pease Limitation" when it came to itemized deductions. I won't go into detail on the Pease Limitation here but TCJA suspended that provision in 2018. Moreover, OBBBA permanently repealed the Pease Limitation but replaced it with a new limitation for higher earners in the 37% bracket when it comes to itemized deductions starting in 2026.

Under OBBBA the new limitation reduces itemized deductions by 2/37 of the lesser of:

- The taxpayer's total itemized deductions (yikes!)

- The amount by which their taxable income, including itemized deductions, exceeds the 37% bracket (before the limitation applies)

The reason for this is that the bill is essentially aiming to reduce the benefit of itemized deductions for the highest earners.

Here's an example:

Let's say you're a married couple and you have $850,000 in AGI. You also have $175,000 in itemized deductions.

Under TCJA, you would be able to deduct all $175,000 of your itemized deductions against your AGI, reducing your taxable income to $675,000 ($850,000-$175,000).

Under OBBBA, your allowable itemized deductions would be reduced by 2/37 of the lesser of $175,000 (itemized deductions) or $98,400 ($850,000 [AGI] - $751,600 [37% bracket threshold]). In this example your itemized deductions would be reduced by 2/37 of $98,400 = $5,319 leaving you with allowable itemized deductions of $169,681 and a taxable income of $680,319.

OBBBA made the Qualified Business Income (QBI) deduction permanent. For business owners this is great news since the QBI deduction was set to expire at the end of 2025.

The QBI deduction is a deduction that was created by TCJA in 2018 and it is, in simplistic terms, a 20% deduction of net business income for pass through entities like sole proprietors, single member LLCs, partnerships and S-Corps. This deduction is in addition to the standard or itemized deduction available to taxpayers as well.

The deduction calculation can be a little more nuanced and complicated depending on your taxable income and if your business is a specified service trade or business (SSTB), like a lawyer, accountant, athlete, etc., or a non-SSTB, but this is a nice deduction for self-employed taxpayers and business owners.

As with most provisions in the tax code there are income limits with this deduction.

Currently, if your taxable income is over the thresholds ($197,300 for single taxpayers and $394,600 for married taxpayers filing jointly) then you are subject to a phaseout. Within the phaseout range then your QBI deduction begins to be reduced for both SSTBs and non-SSTBs. Once your income is $50,000 (single) or $100,000 (married) over the applicable thresholds then your QBI deduction is eliminated for SSTBs.

Under OBBBA, the income thresholds are still the same but the phaseout ranges are now $75,000 (single) and $150,000 (married).

The QBI deduction is another area that has a lot of complexity and it's important to work with your tax professional to help you navigate and optimize this deduction.

When it comes to your taxes there are what's called "above-the-line" deductions and then the Standard/Itemized deductions. With the onset of the QBI deduction there are now also "below-the-line" deductions which are deductions to your income after "above-the-line" deductions and the standard/itemized deductions. These deductions lower your taxable income but do not lower your AGI like "above-the-line" deductions. This is an important distinction since AGI is used for qualifying for many provisions of the tax code (Roth contributions, IRMAA, etc.).

OBBBA introduced quite a few new "below-the-line" deductions.

No Tax on Tips

There was a lot of talk and anticipation around tax legislation that may remove tax on tip income and OBBBA came through on some of that.

*It's important to note that while OBBBA did eliminate income tax on qualified tip income, tip income is still subject to payroll tax, included in AGI and may also be subject to state income tax depending on your state.

Under OBBBA you can deduct up to $25,000 of qualified tip income (same deduction amount for single or married filers). This deduction also has an income phaseout that begins at MAGI $150,000 for single filers and $300,000 for married filing joint filers.

To have any tip income qualify for the deduction there are also a few rules in place:

- The taxpayer must work in an occupation that "traditionally and customarily" received tips before 2025.

- The tips must be voluntary and not mandated as part of the service being provided.

- The tips can't be earned through an SSTB

No Tax on Overtime Pay

Similar to the no tax on tips provision, there is a deduction for qualified overtime pay as well from 2025-2028. Unlike the qualified tip deduction, the qualified overtime pay deduction is $25,000 for married filers and $12,500 for single filers.

However, the phaseout range and rules are the same with the phaseout starting at MAGI $150,000 for single filers and $300,000 for married filing joint filers.

Auto Loan Interest Deduction

Another new "below-the-line deduction" under OBBBA is the auto loan interest deduction, again effective for tax years 2025-2028.

The deduction applies to new (not used) vehicles (cars, vans, SUVs, pickup trucks and motorcycles) for personal use (not business use), and the loan for the new vehicle must be originated after December 31, 2024. Additionally, the vehicle must have been manufactured in the US.

The deduction is limited to $10,000 of total loan interest and of course has MAGI limitations.

The phaseout for this deduction begins at MAGI $100,000 for single filers and $200,000 for married filing joint filers and the deduction is completely phased out for MAGI $149,000 for single filers and $249,000 for married filing joint filers.

Charitable Deduction

Most of the time to be able to deduct your charitable contributions you would need to itemize your deductions. OBBBA brought back a charitable deduction for people who don't itemize their deductions.

Under OBBBA single filers can deduct up to $1,000 and married filers can deduct up to $2,000 of charitable donations "below-the-line" if they don't itemize.

This charitable donation deduction is not subject to the 0.5% floor that is applicable to itemized charitable donation deductions.

The child tax credit was set to decrease back to $1,000 per child from $2,000 at the end of the year. However, OBBBA permanently increased the child tax credit to $2,200 for 2025 and then has the credit indexed to inflation every year thereafter starting in 2026.

OBBBA also maintains the MAGI phaseouts for this credit at $200,000 single and $400,000 joint.

Other various changes

There are several other changes in OBBBA such as changes to the Alternative Minimum Tax (AMT), eligible 529 expenses, health savings accounts (HSAs), the estate tax exemption amount, "Trump" accounts, qualified opportunity zones and Qualified Small Business Stock (QSBS) just to name a few that we won't cover here.

OBBBA was a very long and extensive piece of tax legislation that will impact different people in different ways when it comes to their taxes.

Therefore, working with a tax professional that does tax planning (not just tax preparation) is critical to making sure you are making the most of the tax provisions available to you and to do some planning to try and reduce your taxes, both now and in the years to come, and potentially for generations to come. Taxes are potentially one of the biggest drains on your assets and income, so proper tax planning cannot be ignored and is key to making sure that you and your family keep more of your wealth

If you want help with tax planning in regards to your situation (retirement planning, estate planning, etc.) please reach out to us to set up a complimentary phone call or meeting by clicking the link below.

Best,

Michael Didion

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Didion Wealth Management and LPL Financial does not provide legal or tax advice. Please consult your legal or tax advisor regarding your specific situation.