One of the biggest aspects of retirement planning is knowing where your income in retirement is going to come from. This is an important piece of retirement planning since you obviously won't be working to bring in an income when you're retired and you'll want to know that you have enough income coming in to make sure you'll be ok, hit your goals and live the lifestyle you want in retirement.

Retirement income can come from a variety of sources.

→ Pension income

→ IRAs

→ 401ks and other employer sponsored retirement plans

→ Taxable brokerage and investment accounts

→ Annuities

And, of course,

→ Social Security

Your eventual social security retirement income benefit will likely be one of the biggest pieces of your retirement income plan so it's important to get it right because with most decisions around social security once you make a decision you can't change your mind.

So it begs the question, "What's the best strategy for social security?".

To make sure you get it right you need to know the basics of the different social security retirement income options available to you so you can make the best decision for you and your retirement plan.

This is one of the first, and one of the most critical, social security retirement income strategies for you to be aware of.

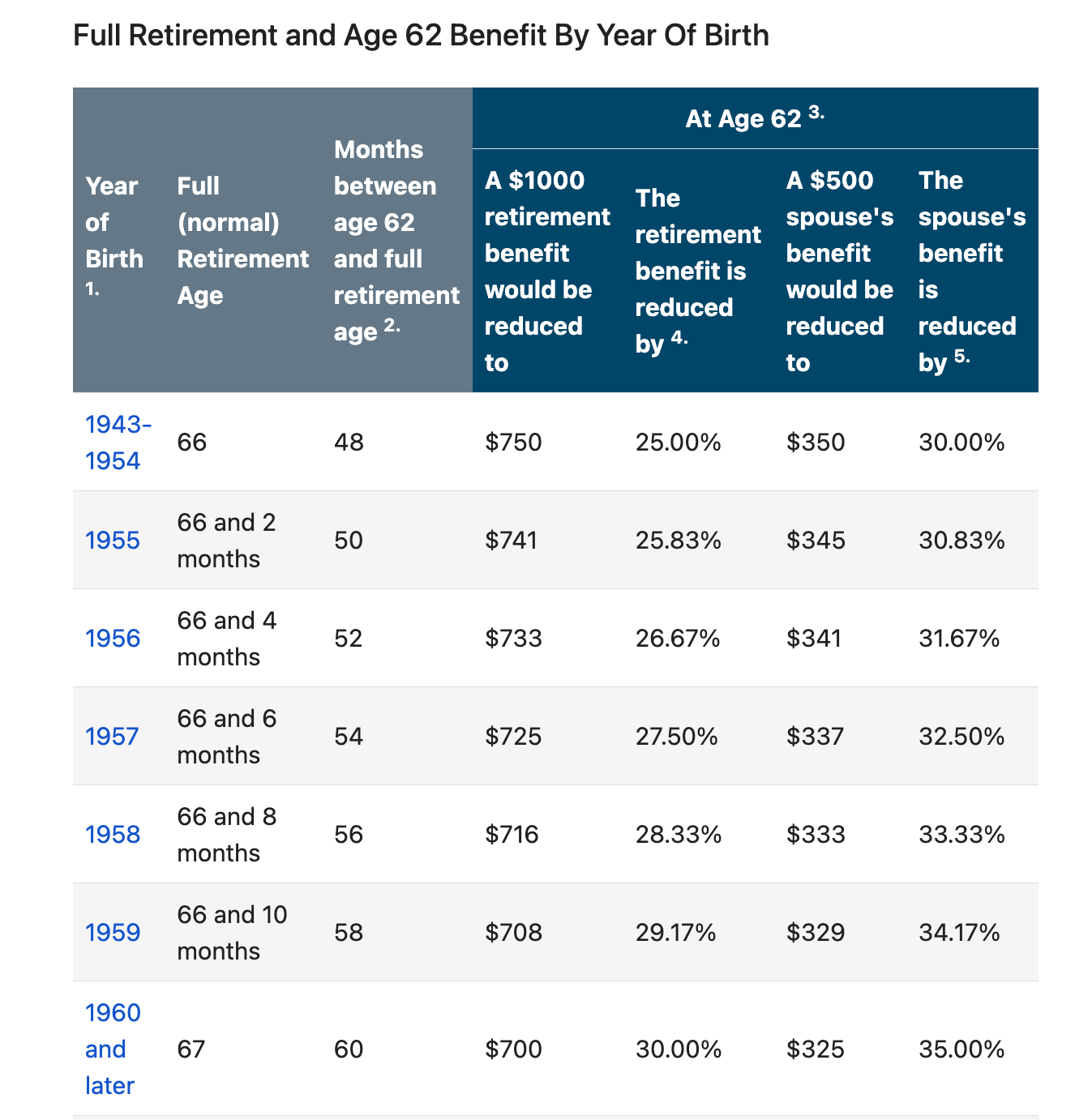

To be able to collect your social security benefit you first need to "file" for your benefit with the social security administration. And if you can receive a benefit, and how much of benefit you are entitled to, depends on your age. What is called your "full retirement age" (FRA) is considered your actual retirement age and the age at which you receive your "full" social security benefit. Currently, the FRA for people born after 1960 is 67. For people born before 1960 there is a different FRA that is younger than age 67.

The earliest you can file for your social security is at age 62. However, if you do this there is a permanent reduction in your monthly benefit. If you elect to take social security early you cannot change your mind and cancel getting your benefit. That's why your benefit is permanently reduced.

On the flip side, you can delay taking social security up until age 70 and have your monthly benefit increased. Waiting until age 70 will max out your benefit and will result in the largest possible social security benefit you can receive.

There's a range for what your monthly benefit would be from age 62 until 70 that varies between what your benefit would be at age 62 and what it would be at age 70.

Figuring out when is the best time for you to file for your benefit takes knowing these numbers and analyzing how it fits into your overall retirement income plan. Maybe it makes sense for you to take your social security at age 62, or maybe it's 65, or maybe you can wait unitl 70.

The answer is unique to you and your individual goals.

Below is the FRA by birth date, as well as the reduction of benefits if you take your social security early.

*source SSA.gov

If you're married, and you're receiving your social security benefit, then your spouse may qualify for a spousal benefit based on your benefit. However, your spouse must be at least 62 years old and, generally, you need to have been married for at least 1 year for your spouse to qualify for a spousal benefit.

The spousal benefit can be up to 50% of your benefit, depending on your spouse's age when they file for their retirement benefit. If your spouse files for benefits at 62, then the benefit is permanently reduced (similar to if you file for your own benefit at age 62). Waiting until your spouse's FRA will allow them to get their full, 50% spousal benefit.

Now, if your spouse has a social security benefit under their own record and it's higher than the spousal benefit, they will receive the higher benefit.

So when your spouse files for their benefit it's important to also file for the spousal benefit. That way the social security office will give your spouse the higher benefit that they qualify for.

Given the different amounts your spouse can get under the spousal benefit or their own benefit, it's important to do some planning and determine when's the best time to file to maximize the social security benefit for your spouse, either under their own benefit or a spousal benefit.

Under social security you may also qualify for survivor benefits, if your current or former spouse dies.

The survivor benefit is based on the deceased spouse's work history and their social security benefit.

To qualify for survivor benefits as an ex-spouse you must be at least age 60, or 50 if you have a disability, and you also must have been married to the deceased spouse for at least 10 years and not have remarried before age 60.

The amount of your survivor benefit you receive can be between 71.5% and 100% of your deceased spouse's benefit. The longer you wait to take the survivor benefit the higher your benefit will be, maxing out at 100% of your deceased spouse's benefit at your full retirement age.

The social security office recommends you contact them right away when your spouse dies to discuss the options you have available to you. While that's not a bad idea it's important to know your options and which option is the best for you before you call the social security office.

For example, you may want to take the survivor benefit instead of taking your benefit (or delaying taking your benefit) if the spousal benefit is higher, or take your reduced benefit first and then wait to take the higher spousal benefit later.

Either way, it's important to know your options and pick the best one for you and your situation, accounting for other sources of income and retirement assets you have, as well as any retirement goals you have.

Similar to spousal benefits, if you're divorced you may be entitled to receive a spousal benefit under your ex's work record if you meet certain conditions.

The conditions you need to meet are:

→ You and your ex must have been married for at least 10 years.

→ Both you and your ex must be at least age 62.

→ You must not currently be remarried.

Additionally, you can receive benefits if you have been divorced for 2 years and your ex has not filed for benefits but is able to file.

So, how much can you get as a divorced spouse?

If you qualify, you can get up to 50% of your ex's benefit even if your ex has remarried.

When you go to file for social security benefits, you'll receive your own social security benefit first. And if it's less than 50% of your ex's benefit then you'll get an additional amount that when totaled together with your own benefit will equal 50% of your ex's benefit.

When you file, it's important to let the social security office know that you may qualify for the divorced spousal benefit.

Another important consideration is that your ex must have reached their FRA for you to qualify for the full 50% divorced spouse benefit.

The best option for social security will obviously depend on your situation.

You need to know at what age you'll file social security and what different benefit options you have (spousal, divorced spouse).

Figuring out at what age to file is a huge part of the equation and determining at what age to file takes some planning and analysis. You'll want to consider...

→ Your other sources of retirement income (pensions, annuities, etc.)

→ What retirement assets you have to supplement your retirement income (401ks, IRAs, taxable accounts)

→ How much you'd like to spend in retirement

→ How much your social security benefit would be at various ages (62, 65, 67, 70)

→ What's your spouse's benefit

→ Life expectancy of you and your spouse

At what age you file also impact other benefits such as spousal benefits so it can't be stressed enough how important it is to do some planning around when you file.

Don't just wing it.

If you haven't done any retirement planning and need help figuring out when to take your social security benefit, feel free to reach out my office for a complimentary discovery call to see how I can help you.

Cheers,

Michael